Private soirée

Posted on March 1st, 2016 – Comments Off on Private soirée

…sometimes someone hears you.

An Open Letter to Canadians

RBC has been in the news this week in a way no company ever wants to be.

The recent debate about an outsourcing arrangement for some technology services has raised important questions.

While we are compliant with the regulations, the debate has been about something else. The question for many people is not about doing only what the rules require – it’s about doing what employees, clients, shareholders and Canadians expect of RBC. And that’s something we take very much to heart.

Despite our best efforts, we don’t always meet everyone’s expectations, and when we get it wrong you are quick to tell us. You have my assurance that I’m listening and we are making the following commitments.

First, I want to apologize to the employees affected by this outsourcing arrangement as we should have been more sensitive and helpful to them. All will be offered comparable job opportunities within the bank.

Second, we are reviewing our supplier arrangements and policies with a continued focus on Canadian jobs and prosperity, balancing our desire to be both a successful business and a leading corporate citizen.

Third, our Canadian client call centres are located in Canada and support our domestic and our U.S. business, and they will remain in Canada.

Fourth, we are preparing a new initiative aimed at helping young people gain an important first work experience in our company, which we will announce in the weeks ahead.

RBC proudly employs over 57,000 people in Canada. Over the last four years, despite a challenging global economy, we added almost 3,000 full-time jobs in Canada. We also hire over 2,000 youth in Canada each year and we support thousands more jobs through the purchases we make from Canadian suppliers. As we continue to grow, so will the number of jobs for Canadians.

RBC opened for business in 1864 and we have worked hard since then to earn the confidence and support of the community. Today, we remain every bit as committed to earning the right to be our clients’ first choice, providing rewarding careers for our employees, delivering returns to shareholders who invest with us, and supporting the communities in which we are privileged to operate.

I’d like to close by thanking our employees, clients, shareholders and community partners for your input and continued support.

Sincerely,

Gord Nixon

President and Chief Executive Officer,

Royal Bank of Canada

I know I’ve spent a lot of time pissing on the Conservatives and Harper, but it’s become exceedingly obvious that the Liberals are just more of the same, the same broken system of bipartisanship designed to keep us all arguing on the ground instead of looking at the houses of power and seeing the truth of the corruption and lies being peddled there.

I say this because of Dalton McGuinty’s latest revelation that his budget, which he wants the NDP to guarantee in writing to vote for, includes a section that would privatize ServiceOntario. In case you’re wondering what this agency does, here’s a quick rundown of everything that would fall into private hands:

All this even as, in the same budget, McGuinty’s government boasts about how they’ve saved $1.5 billion last year. So how do they justify it? With the claim that Canada is poor because of the 2009 recession, and we need to cut cut cut! This is probably thanks to Harper (may I have a second helping, sir?), even though the Liberal’s own website strongly suggests this is not the case.

In any event, the Libs are holding up the construction and almost immediate sale of highway 407 as the type of resounding success that privatization can bring. I’m sure anyone who takes the 407 is familiar with just how amazing it is to be under the yoke of a private agency that can revoke your driving privileges. And wasn’t it the Libs who took the 407 to court to try to break that contract? And, what a wonderful example to hold up anyways…the fact that it cost over $100 billion to build, land acquisitions and all, and was sold for just over $3 billion for a quick $1.5 billion “profit” for the Conservatives that wasn’t really a profit at all.

Look, I get it, all of you who have been calling these people “Fiberals” have, I admit, been far too kind about your monickers, but just don’t delude yourselves that by being on the other side (ergo the Conservatives), is any better. The government at all levels (I’m sure I’ve mentioned my municipal government more than once), seems hell bent on robbing citizens blind for the benefit of the banks. A global deficit, after all, is impossible if the same money lent out is what’s owed — that’s just elementary logic. The only way that the whole world can owe an approximate $200 trillion is if someone either stole that amount, or loaned it out fraudulently (they never had it to begin with), and is now expecting payback. And I dunno know about you, but the government only ever takes my money, never gives me any, so I sure as hell wasn’t on the receiving end of any such “loan”.

The fact that politicians are all mentioning that the “new” deficit is going to come from Europe where it was caused by banks lending out money they didn’t have (with much help by Government laws and regulations), and then expecting payback for cash literally created out of thin air (look up “fractional reserve banking” if you need an explanation), indicates a strong collusion, probably even big kickbacks (but how would we know? The banks control the money supply!) Besides, haven’t governments been handing over taxpayer money to the banks by the billions to solve this “problem”? How’s that been working out?

So doesn’t it just make perfect sense to go in exactly this direction more and more? Then, when we can’t pay our “debts” anymore, the banks can just privatize everything and then get ready for some genuine old-school slavery (or feudalism if you like, and if we’re lucky). And the government can be expected to back them all the way.

I recently had a situation where one of the cheques I wrote bounced. Happens. But what I discovered as a result shocked and upset me.

They’re charging me $42.50 for a bounced cheque!

For starters, I wanted to know who I could contact about my bank. I visited the OBSI website and discovered that my institution decided it just simply didn’t want to participate anymore. According to OBSI, this means:

Unfortunately, some financial services providers are not covered by an ombudsman service.You may have to contact a government department or regulator if you are dealing with a mortgage broker, insurance broker, financial planner or other service which is not covered by an ombudsman. Some resources to help you can be found in our Useful Websites.

Didn’t help much except to give me the TD Ombudsman’s email address. So I shot off an email:

Hello Mr. XXX,

I’ve recently managed to run into an NSF situation with my chequing account due to an error on my part. I noticed that the NSF fee has been increased to $42.50, a sum I don’t recall ever being informed about. In regards to NSF fees, I have a couple of questions and a complaint to make:

Questions

- How does BANK determine the fee of $42.50? This value seems incredibly high and fairly arbitrary considering most of the clearing process is completely automated (it would seem that the only costs incurred would be for the electricity consumed and perhaps the decreasing cost of the computer equipment involved).

- What is BANK’s responsibility in informing customers in NSF fee increases? And what are the repercussions to BANK for simply arbitrarily setting any fees it likes – what laws govern this? I’m presuming the standard placations that BANK “wouldn’t do that” (a need to retain customers, fairness, etc. etc.), but given that this is precisely what is being done, not to mention my own experiences and knowledge working behind the scenes at financial transaction networks, I would appreciate a forthright explanation.

Complaint

Banks, including BANK (I believe), currently charge the depositor for NSF as well ($20 is my understanding). This fee seems exceptionally egregious since the depositor has absolutely no control over what funds may or may not be in the cheque issuer’s account. This is similar to mobile phone companies who had been charging customers for receiving text messages – when there is no option or ability to refuse – or even know about impending charges — the courts have found such behaviour to be unlawful and has resulted in large fines. From my point of view, the banks seem to be engaging in this practice as well, and it becomes worse when it’s done by a bank where both the cheque issuer and the depositor both have an account – the bank is in the sole position to know that a cheque will be returned NSF and allows for no recourse, thereby seemingly simply taking money from account holders as it likes. And after exacting such exorbitant fees, the bank does not see fit to offer any services that might benefit their customers in such situations, seemingly chalking up the money extracted as nothing more than profits to be shared among shareholders. Is this accurate? And if it’s not, please offer an explanation.

I have a few other points of contention with bank operations but I would like to start with these.

Thanks for your time and attention.

Sincerely,

Patrick Bay

In hindsight I realized I’d unintentionally fibbed a bit — I do get notices that my bank account is being changed, by mail — but it still seems pretty unsavoury that they can just up their fees (note how they never go down), at any time by simply telling you they’re going to do it. It’s kind of like making theft legal so long as the robber lets you know he’ll be dropping by next Tuesday.

And I do feel pretty strongly about calling it theft based on the escalating NSF fees that banks charge, not only to me, but more to the person on the receiving end. Seriously, $20 for receiving a cheque that bounces? As I point out in my letter, mobile carriers did this to consumers with text messages, and the law wisely said that we can’t possibly held accountable for something that’s completely out of our control and even knowledge.

In any event, I can’t help but feel jaded by the knowledge that even though we have a Consumer Protection Act, financial services and banks seem to be completely omitted from it (a.k.a. they’re the only business that the CPA doesn’t really want you to know about). And, sadly, the Bank Act doesn’t do a whole heck of a lot on protecting customers either, though it does spell out all sort of insane rights that no individual would ever have.

Yes, it’s true that I did work behind the scenes at a financial transaction network and saw exactly where most of the bank fees go — into the bankers’ pockets. I sure as heck didn’t get rich working there, and on an average night, a financial institution would walk away with between $1000 to $2000 in pure profit (after I’d been paid, rent was covered, etc.) And this was a tiny side-network of small credit unions that were connected to Interac and decades ago; I can’t imagine the level of skimming on just standard transaction on any given day on something like the whole Interac network or Plus today.

Do you remember what the banks promised to everyone when ATMs were just starting to be rolled out to the public? “Oh, it’ll make things cheaper! Now you won’t have to pay for a teller and all of your transactions will be much smaller!” Yeah, $1.50 to $3.00 a transaction — MUCH cheaper. That was just the beginning of the wholesale lie.

When banks complain that they’re the most regulated industry out there, maybe it’s because they need to be. Maybe because they’re the most crooked, the most in need of control. Maybe as consumers we need take control back since the government seems only too happy to give it away, and the banks are only too happy to abuse it.

Rob Ford, Dalton McGuinty, and Stephen Harper are all into the austerity game. Oh yeah, we all lived way beyond our means and it’s time to start paying back!

Except guess what…it’s an unbelievable scam being perpetrated by the big banks that’s bankrupting our economy, not any of our social programs, our schools, our libraries, our garbage collection…

I think it’s about time to start electing politicians that will:

a) Tell the goddam truth about where our money is really going

b) Stand up to the banking cartels (let’s not mince words, they are criminal enterprises)

If you’re not quite sure, have a gander at this documentary. All the numbers and facts are correct, and none of the stinking politicians seem in the slightest interested in fixing it.

…continued from previous part.

Okay, it’s now been well over two weeks and I’m just about ready to put this puppy to bed.

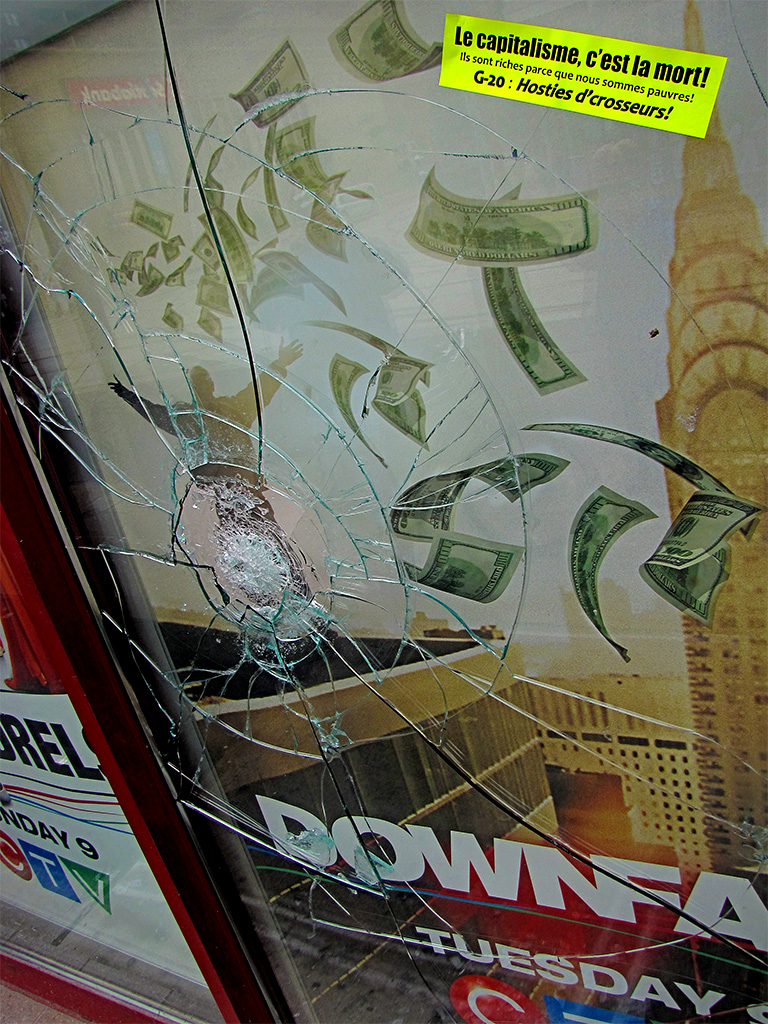

But before I do, let me round out the G20 weekend for you, dear reader. Let’s start with the Black Bloc, the attention whores of the summit. While I was trying to figure out who they are and where they came from, a few glaringly obvious pieces of evidence jumped out at me with a, “zut alors!”